Pros and Cons of Multiplan Insurance remain a critical healthcare discussion in 2025- but here’s the twist: Multiplan isn’t actually insurance. This fundamental misunderstanding fuels consumer confusion and frustration nationwide. Imagine paying premiums for what you believe is comprehensive coverage, only to discover your “PPO plan” covers barely 15% of your surgery bill. Recent FTC crackdowns reveal how marketers have deceptively sold limited-benefit products as “Multiplan insurance,” leaving patients with junk coverage and provider nightmares. With Multiplan’s recent rebrand to Claritev promising transparency and fairness, does 2025 mark a turning point? We dissect the complexities with real cases, regulatory updates, and frontline provider experiences to empower your healthcare decisions.

Contents Skip Ahead

- 1 What Exactly is Multiplan?

- 2 The Advantages: Why Multiplan Persists

- 3 The Hidden Drawbacks: 2025 Realities

- 4 Multiplan in 2025: The Claritev Rebrand

- 5 Who Should Consider Multiplan-Affiliated Plans?

- 6 Critical Questions to Ask Before Enrolling

- 7 The Future: Regulatory Crackdowns Loom

- 8 Q&As on Multiplan Insurance

- 9 Conclusion: Pros and Cons of Multiplan Insurance

What Exactly is Multiplan?

The Middleman Model

Multiplan (now Claritev) serves as a negotiation intermediary between insurance companies and healthcare providers. When you see “PPO” on your insurance card with Multiplan’s logo, it means your insurer contracts with Multiplan’s network of over 1.4 million providers to secure discounted rates.

How the System Works

- Out-of-network claims get routed to Multiplan

- Multiplan analyzes the bill and proposes a “fair” payment

- Providers either accept this rate or balance-bill patients

- Insurers and Multiplan share fees based on the “savings” generated

2025 Development: Multiplan’s February 2025 rebrand to Claritev emphasizes their evolution into a “healthcare technology, data and insights company,” though core services remain unchanged.

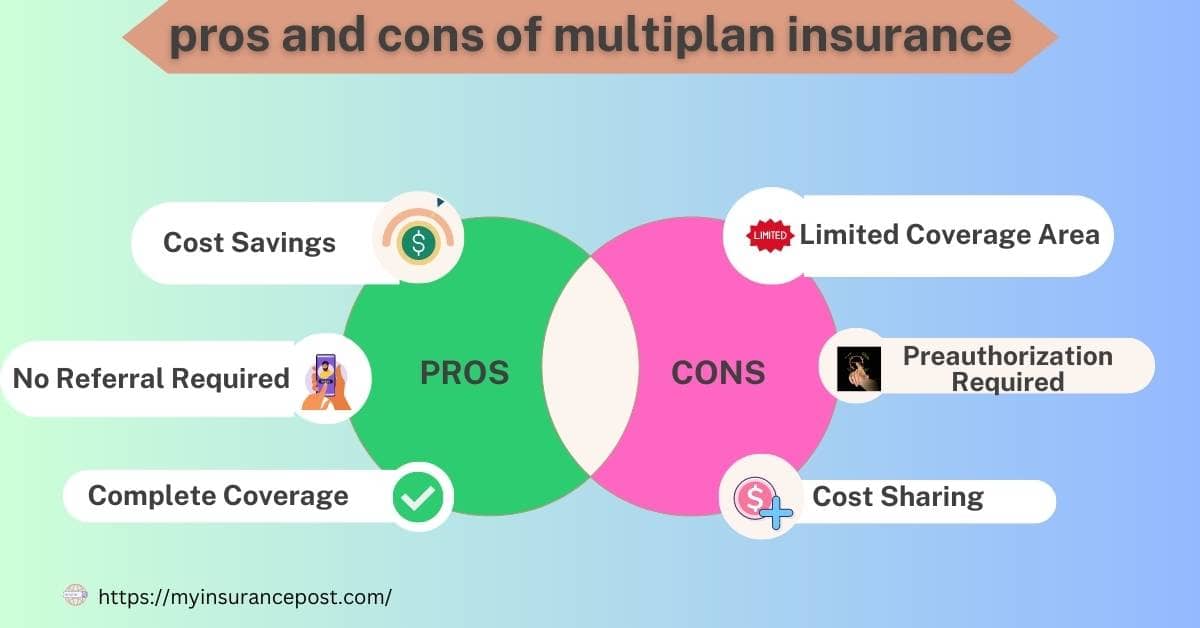

The Advantages: Why Multiplan Persists

1. Extensive Provider Choice

- Largest PPO network in America with 700,000+ doctors

- No referrals needed for specialists

- Nationwide coverage benefits travelers and multi-state residents

Real Impact: A Chicago-based consultant with chronic conditions reported: “With Multiplan’s PHCS network, I found specialists in 12 states during my travels last year without claim denials.”

2. Potential Cost Savings

- Negotiated discounts of 30-70% on medical services

- Preventive care coverage in comprehensive plans

- No surprise bills when providers accept Multiplan’s rate

3. Flexibility for Self-Funded Employers

- Large employers like Fortune 500 companies use Multiplan to manage out-of-network costs

- Customizable networks based on workforce needs

- Data analytics for cost forecasting

The Hidden Drawbacks: 2025 Realities

1. Misleading Marketing of “Junk Plans”

The FTC’s $100 million settlement with Benefytt Technologies exposed systemic deception:

- Telemarketers sold limited-benefit plans as “PPO insurance through Multiplan”

- Consumers told “every doctor accepts this” faced rejected claims and unrecognized coverage

- 40% agent commissions incentivized fraudulent sales

Victim Example: Jeremy Rios purchased a “PHCS universal Multiplan PPO” plan after being promised “$0 deductible” and universal acceptance. He later discovered no local providers honored it, triggering a cancellation battle.

2. Problematic Provider Compensation

Multiplan’s percentage-based pricing model creates perverse incentives:

- Providers must inflate billed charges to receive reasonable payments

- Reducing charges triggers disproportionate payment cuts

Case Study: A surgery center biller lowered a procedure charge from $32,000 to $4,500 seeking fairness. Multiplan’s offer plunged from $3,539 to $673- a 90% reduction. When he rebilled at $28,000, payments rose to $2,548.

3. Patient Cost Uncertainty

- Physical therapy costing $400/session might only get $151 credited toward deductibles

- 10 PT sessions could cost patients $3,800 vs. $2,320 under non-Multiplan plans

- Balance billing remains legal in most states when providers reject Multiplan’s rate

4. Opaque Claim Repricing

A 2024 New York Times investigation revealed:

- UnitedHealthcare, Aetna, and Cigna use Multiplan to systematically slash out-of-network payments

- Fees to insurers/Multiplan often exceed actual medical reimbursements

- Patients face higher bills as payments nosedive below actual costs

Multiplan in 2025: The Claritev Rebrand

What Changed (and What Didn’t)

- New identity: Claritev Corporation (ticker: CTEV)

- Same services: Network access, claims repricing, cost containment

- Expanded focus: AI-driven data analytics and “healthcare transparency”

Unresolved Issues

- BBB complaints persist about harassment and billing disputes

- Providers report continued unwanted negotiation contacts despite opt-out requests

See Also: How to Scare Insurance Adjuster: Tips to Maximize Your Claim 2025

Who Should Consider Multiplan-Affiliated Plans?

Potentially Suitable For:

- Healthy individuals needing catastrophic-only coverage

- Employer groups with strong benefits administrators

- Cash-based practices willing to accept deep discounts

Likely Poor Fits:

- Chronic illness patients needing consistent specialist care

- Low-income households vulnerable to balance bills

- Providers valuing autonomous rate setting

Critical Questions to Ask Before Enrolling

- Is this actual insurance or a limited-benefit plan using Multiplan’s network?

- What percentage of my hospital bill would this cover for emergency surgery?

- Can you show me in-writing examples of claims payouts for my medications?

- What are the shared savings fees charged to my employer?

The Future: Regulatory Crackdowns Loom

- Department of Labor investigations requested into insurer-Multiplan pricing collusion

- FTC scrutiny of deceptive marketing continues post-Benefytt settlement

- HHS rulemaking expected on short-term limited-duration (STLD) “junk” plans

Q&As on Multiplan Insurance

Q: Is “Multiplan Insurance” real insurance?

A: No. Multiplan (now Claritev) is not an insurer. It’s a PPO network manager and claims repricing company. Beware of limited-benefit “junk plans” deceptively marketed as “Multiplan insurance,” which were the focus of the FTC’s $100 million settlement in 2024.

Q: Why do providers complain about Multiplan payments?

A: Multiplan uses a percentage-based model. If providers lower their billed charges seeking fairness, Multiplan slashes payments disproportionately (e.g., a 90% payment cut for a 86% charge reduction). This perversely incentivizes inflated initial bills.

Q: Can patients still face surprise bills with Multiplan?

A: Yes. If your provider is out-of-network and rejects Multiplan’s repriced offer, they can balance-bill you for the difference. This remains legal in most states, leading to unpredictable out-of-pocket costs despite “network discounts.”

Q: What changed with the rebrand to Claritev in 2025?

A: The core service (network access, claims repricing) remains the same. Claritev emphasizes new data analytics/AI tools and “transparency,” but provider complaints about unwanted negotiations and patient confusion over coverage persist.

Q: Are regulators taking action against Multiplan practices?

A: Yes. Following the FTC crackdown on deceptive marketing, the Department of Labor is investigating potential collusion between insurers and Multiplan to underpay claims. HHS is also expected to tighten rules on short-term “junk” plans using such networks.

Conclusion: Pros and Cons of Multiplan Insurance

Multiplan- now Claritev- occupies a complex, controversial niche in American healthcare. While its PPO network offers unparalleled breadth, 2025’s realities demand caution: deceptive marketing traps, unpredictable patient costs, and provider payment models that incentivize billing inflation remain entrenched challenges.

For consumers: Verify plan details beyond the “Multiplan/PHCS” logo. Demand written coverage examples.

For providers: Audit payments for percentage-based patterns. Document all opt-out requests.

For employers: Scrutinize “shared savings” fees that may encourage claim underpayment.

As regulatory storms gather, Claritev’s promised “transparency revolution” faces its first real test. The path forward must bridge the gap between corporate profitability and healthcare fairness—because when middlemen profit from payment disputes, patients and providers lose.